A futures contract is a standardized contract to buy or sell specific quantities of a specified commodity of standardized quality on a certain date in the future and at a market-determined price, i.e., the futures price. These contracts are traded on a futures exchange.

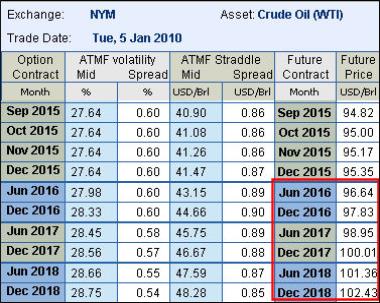

On any given date you can see a number of future contracts ahead, i.e., you can see the future contracts out to the last quoted future contract on a certain date. However, the further ahead in time you get from the current date, the less future contracts are available. For example, for the Crude Oil asset traded on NYMEX on any given date you can see the monthly future contracts for the next 5 years and then for years 6-8 you can only see the June and December contracts, as seen in the Term Structure page in See "Available Future Contracts Displayed in the Term Structure ".

Figure 1: Available Future Contracts Displayed in the Term Structure

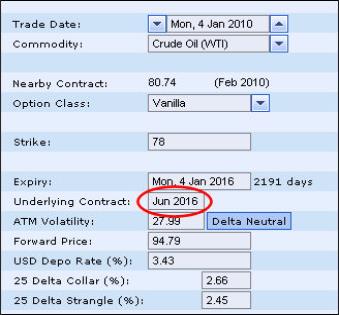

Accordingly, if on 4 January 2010 you price a 6y vanilla option on Crude Oil, the nearest underlying future contract available will be the Jun 2016 contract (as seen in See "Nearest Underlying Future Contract Is Always Displayed ").

Figure 2: Nearest Underlying Future Contract Is Always Displayed

However, for all exchange traded energy assets (i.e., Brent Crude Oil, Crude Oil, Gas Oil, Heating Oil and RBOB Gasoline) you can instruct SDX Commodities & Energy to automatically interpolate the future price for any missing future contracts up until the commodity's last quoted future contract.

Once SDX Commodities & Energy has interpolated the missing future contracts for a specific asset it:

Adds them to the asset's term structure page.

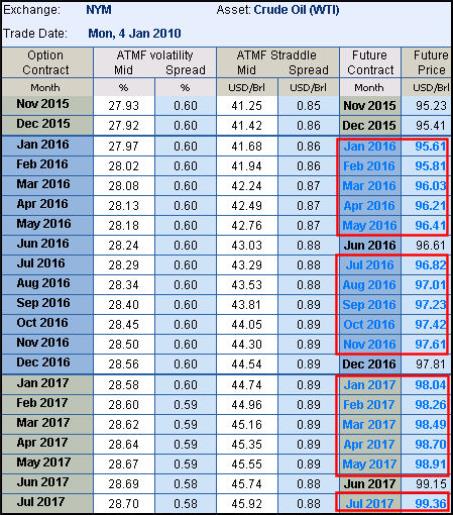

In the Term Structure page any system interpolated future contracts (and their future prices) are highlighted in blue to indicate that they have been interpolated by the system. This makes it easy for you to see which future contracts are interpolated and which actually exist in the market.

So continuing the example above, on 4 Jan 2010 for the Crude Oil asset traded on NYMEX the system will automatically fill in the missing monthly future contracts (i.e., Jan, Feb, Mar, Apr, May, Jul, Aug, Sep, Oct and Nov) for years 6-8 (i.e., 2016, 2017 and 2018). You can see these interpolated contracts in the asset's term structure page in See "Interpolated Future Contracts in the Asset’s Term Structure ".

| Figure 3: | Interpolated Future Contracts in the Asset’s Term Structure |

Uses this data to price instruments as relevant.

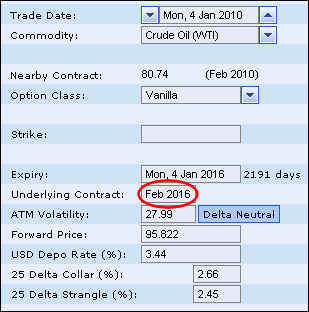

So if you instruct the system to interpolate the missing contracts and then on 4 January 2010 you price a 6y vanilla swap on Crude Oil, the nearest underlying future contract available will be the Feb 2016 contract (as seen in See "Instruments Can Be Priced Using Interpolated Future Contracts ").

| Figure 4: | Instruments Can Be Priced Using Interpolated Future Contracts |

It is important to note that:

This feature is not enabled for your user by default. You must activate for your user via the Customize window.

The system interpolates the future contracts that are missing for the current trade date. So if on the 4 Jan 2010 you enter a historical trade date of 4 Jun 2009 the system will interpolate the future contracts that are missing in the system on 4 Jun 2009, i.e., Jan, Feb, Mar, Apr, May, Jul, Aug, Sep, Oct and Nov for 2015, 2016 and 2017. These will not be the same future contracts that it interpolates for 4 Jan 2010.

To enable this functionality:

| 1. | On the ribbon bar in the Home tab click the Settings button. |

| 2. | In the Customize window, click the Term Structure tab. |

| 3. | In the Define Term Structure area click the relevant checkbox to indicate the period for which you want SD to interpolate the missing future contracts. |

Why is this feature useful? Whereas some users prefer to base their pricing only on data that really exists in the market, others consider it more accurate to interpolate the missing data and to use it in the pricing of instruments as relevant.