An instrument with an uneven maturity is one whose life span does not divide exactly into the chosen coupon periods. For example, you have a quarterly roll frequency and the instrument’s life span is not divisible by 90 days; this leaves you with a broken accrual or non-regular accrual period. This irregular period or uneven maturity is also known as a stub period.

A stub period can fall at the beginning of the instrument, at the end, or be split over the beginning and the end. In addition, it can be either of the following:

A long stub: The coupon is longer in tenor than the given frequency (i.e., 90 days in our example).

A short stub: The coupon is shorter in tenor than the given frequency.

By default the stub period is assigned to the beginning of the instrument, and it is set to be a short stub. However, you can change these settings to suit your requirements. In addition, as soon as you instruct the system that you want to split the uneven maturity over the first and last stub (which you do by choosing a setting for both the First Stub and the Last Stub fields), then you can also define the length of each of these stubs. You do this by defining the end date of the first stub or the start date of the last stub.

You can control the stub policy in the Cash Flow Dates window.

It is also important to note that for each instrument with an underlying floating leg, by default, how the rate for any stub period in that leg is set depends on market convention—this is true for both a fixed (historical) or implied (future) rate. You can, however, then change the default setting if required. For instructions on how to do this (as well as a list of the instruments for which you can control this setting), see Changing the Rate Setting for a Floating Leg’s Stub Period.

To define which stub is used for an instrument with an uneven maturity:

| 1. | In the pricing page, enter the term of the instrument. |

| 2. | Click the Cash Flow & Dates button to open the Cash Flow Dates window. |

| 3. | In the First Stub and Last Stub dropdown lists choose the required settings. |

| 4. | Set the end date of the first coupon or the start date of the last coupon. |

|

|

You can only define this information if you have chosen to split the uneven maturity over two stubs, one at the beginning and one at the end. |

| 5. | Click Accept. |

Changing the Rate Setting for a Floating Leg’s Stub Period

For each instrument with an underlying floating leg, how the rate for any stub period in the floating leg is set depends on market convention.

That is, depending on the market convention:

The fixing rate for a stub period can be either set to the defined index on the relevant fixing date or it can be a linear interpolated rate based on the instrument’s reference rate (e.g., LIBOR or EURIBOR) fixings.

For the implied rate for a stub period, SD can interpolate it based on either one or two yield curve(s), as relevant for the given stub period, or simply always use a single yield curve.

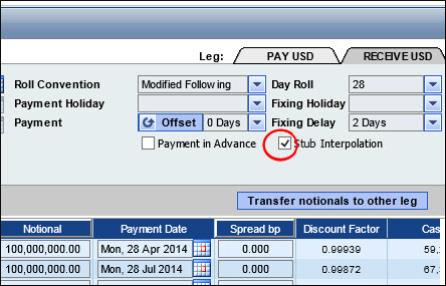

The setting is controlled using the Stub Interpolation checkbox in the Cash Flow & Dates window for the floating leg (as seen in Figure 1).

|

|

This checkbox is only displayed for the floating leg of an instrument and only then if SD allows the user to change the market convention for how the rate is set. |

Figure 1: Controlling the Rate Setting for a Floating Leg’s Stub Period

If this checkbox is checked, then:

For a historical fixing rate, SD interpolates the rate for the floating leg’s stub period based on the instrument’s reference rate fixings (by checking the checkbox) or to set it to the defined index rate instead (if the checkbox is unchecked).

For an implied rate (i.e., a future fixing rate), SD interpolates the rate based on either one or two yield curve(s), as relevant for the given stub period. So, for example, if the stub period is 2 months, SD uses both the 1M and the 3M yield curves; if the stub is for more than a year, SD uses only the 12M curve, etc.

If this checkbox is unchecked, then:

For a historical fixing rate, SD sets the rate for the floating leg’s stub period to the defined index rate (instead of interpolating it).

For an implied rate, only a single yield curve is used.

For the following instruments, by default the checkbox is checked—that is, a fixing rate for the stub period of the floating leg is a linear interpolated rate based on the instrument’s reference rate (e.g., LIBOR or EURIBOR) fixings and an implied rate is based on the relevant yield curves:

Vanilla swap

Single leg of a vanilla swap

Cross currency swap where the floating leg(s) are based on a vanilla swap

Zero coupon swap

Quanto swap

UF swap

UDI swap

IMM swap

Swaption with an underlying vanilla swap

Forward swaption/Bermudan swaption/swaption straddle strategy/swaption collar strategy/swaption strangle strategy/swaption spread strategy

CMS swap, but not for the CMS leg

CMS spread swap, but not for the CMS leg

Callable swap

Range accrual swap

Inverse floater swap, but not for the structure leg

Callable inverse floater swap, but not for the structure leg

Capped floater swap, but not for the structure leg

Callable capped floater swap, but not for the structure leg

Callable zero coupon swap

CMS range accrual swap, but not for the structure leg

Swap TARN, but not for the structure leg

Inverse floater TARN, but not for the structure leg

Digital swap

Snowball, but not for the structure leg

Reverse snowball, but not for the structure leg

CMS spread range accrual swap, but not for the structure leg

Callable range accrual note

Callable inverse floater note

Currency linked swap

Currency linked swaption

Cross currency linked swap

Currency linked quanto swap

For the following instruments, by default the checkbox is unchecked—that is, a fixing rate for the stub period of the floating leg is set to the defined index on the relevant fixing date and an implied rate is always taken from a single yield curve:

General swap

Swaption with an underlying general swap

Cross currency swap where the floating leg(s) are based on a general swap

For each of these instruments on an individual basis you can, however, instruct SD to change the rate setting by checking or unchecking the checkbox as required.

Why is this functionality useful? Being able to change the stub’s rate setting gives you more flexibility when pricing the instrument, for example, if you want to enter into a hedge based on the index rate or if the stub period is just a few days different from the chosen coupon period.