For all inflation indexes used in an instrument, the system needs to work out the index on a particular day.

For most of the inflation indexes, the same index value is used from one roll date up to the next roll date, i.e., linear day-on-day (intra-month) interpolation is not used. However, some of the inflation indexes—the USD index and the two French indexes—do use linear day-on-day interpolation. For these indexes, the rate changes across the period from one roll date to the next. That is, the rate is interpolated depending on how many days the index spot date1 falls between the preceding roll date and the succeeding roll date.

For the indexes which do use linear inter-month interpolation:

If the index spot date equals the index roll date (which is always the 1st day of a month), then the reference index is exactly equal to the index for the calendar month that falls a certain number of months (as defined by the lag period) prior to that month.

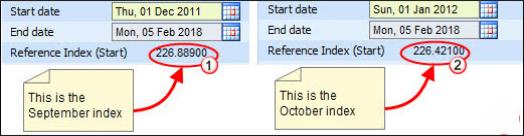

Taking an example of USD, if the index trade date is 29 November 2011, the index spot date is 1 December 2011, which also exactly matches the index roll date. Therefore the reference index used is the reference index for the month of December minus the lag. So if you use the default lag of 3 months, the reference index used is the reference index for September 2011 (as seen at 1 in Figure 1).

The reference index when the index spot date falls on any other day in the month is calculated by linear interpolation between the reference index applicable to the first day of the month in which the index spot date falls and the reference index applicable to the first day of the month immediately following.

So if the lag period is set to three months, the rate is interpolated based on the 3m-2m inflation lag (measured backwards from the trade date).

The linear interpolation is calculated as a weighted average of the two relevant reference indexes, where the weights are as follows:

The weight on the reference index applicable to the first day of the month in which the day falls is calculated as follows:

(D-t+1)/D

The weight on the reference index applicable to the first day of the month immediately following is calculated as follows:

(t-1)/D

Where:

D is the number of days in the calendar month in which the reference index falls.

t is the calendar day corresponding to the date for which you want to calculate the reference index.

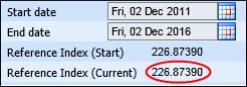

So, continuing the above example of USD, if the trade date is 1 day later, i.e., Wednesday 30 November 2011, then the spot date is Friday 2 December 2011. In this case, the system uses the September and October inflation indexes to calculate the index value. So t=2 (from 2 December), the weights are (31-2+1)/31 = 30/31 and (2-1)/31 = 1/31. The September 2011 index is 226.889 and the October 2011 index is 226.421 (as can be seen at 2 in Figure 1). So the interpolated value is 30/31*226.889 + 1/31*226.421 = 226.8739 (as can be seen in Figure 2).

Figure 1: The Indexes for September 2011 & October 2011

Figure 2: Interpolated Index if the Trade Date Is 30 November 2011

For more details on the index conventions for each supported currency (and its index) see Table 1.

|

For this currency... |

And this index... |

The reference index roll date.... |

Interpolation Type & Default Lag |

|

USD |

USCPI |

Is when the index spot date2 is the 1st of the month. |

Linear interpolation using 3m-2m inflation lag. |

|

EUR |

HICPxT |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 3m. |

|

EUR |

FRCPIxT |

Is when the index spot date3 is the 1st of the month. |

Linear interpolation using 3m-2m inflation lag. |

|

EUR |

HICP |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 3m. |

|

EUR |

ITCPI |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 3m. |

|

EUR |

SPCPI |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 3m. |

|

EUR |

FRCPI |

Is when the index spot date4 is the 1st of the month. |

Linear interpolation using 3m-2m inflation lag. |

|

EUR |

DECPI |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 3m. |

|

GBP |

UKRPI |

Is when the index trade date is the 1st day of the month |

There is no day-on-day interpolation. The default lag is 2m. |

|

AUD |

AUCPI |

Is once every 3 months—on the 15th of March, June, September and December |

There is no day-on-day interpolation. The default lag is 3m. |

|

ILS |

CPI/ILS |

Is the first day after the 15th of the month |

There is no day-on-day interpolation, stepwise with last known index. |