In the IR market an option's premium has traditionally been exchanged on the spot date. However, in September 2010 some of the interbank options markets changed the way premiums are paid for swaptions and swaption strategies.

The new convention defines that a swaption or swaption strategy's premium will now be paid on the option's delivery date (and not on the spot date), i.e., as a forward premium and not as a spot premium.

Why was this change necessary? This change came about as a reaction to the recent financial crisis. As a result of this crisis it became more likely that an instrument seller may default; this not only left a party who had purchased the instrument protection potentially exposed (i.e., without the necessary protection) but also short of the premium that they had already paid for. Accordingly, especially for long term instruments the forward premium convention (i.e., paying the premium at delivery) reduces the risk. This is because, if the other side does default, at least you will not be short the premium as well. In addition, another advantage is that all cash flows are exchanged on one date, i.e., on the delivery date.

In SDX Interest Rates both premium conventions are supported:

In the Single Option page for a swaption and all supported swaption strategies.

This means that when you calculate a supported instrument in the Single Option page, the system automatically calculates the following results for both conventions (i.e., both the spot premium and the forward premium):

Market Price % <currency>

Market Price in <currency>

Theoretical Price

By default the system always displays these results for the spot premium. However, you can choose to toggle between the results calculated for the forward premium and the spot premium using the Premium Spot <> FWD buttons.

This feature is supported in both the Less Details view (-) and the More Details (+) view.

In the Portfolio page for a swaption.

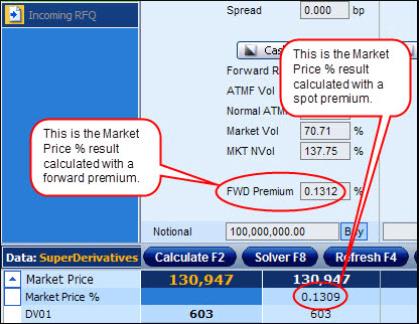

When you price a swaption in the Portfolio page the system calculates the Market Price % result for both the spot premium convention (this is displayed as a mid value in the Market Price % result in the Results area) and for the forward premium convention.

As seen in Figure 1 the market price for the spot convention is displayed as a mid value in the Market Price % result in the Results area and the market price for the forward premium convention is displayed as a mid value in the FWD Premium field in the input area.

| Figure 1: |