An accumulator (acc) is an instrument that lets the investor systematically buy futures in a particular asset from the issuer-where the actual volume and strike used in the payout at maturity are determined over the life of the instrument itself on a series of fixing dates, rather than on the trade date itself.

On each fixing date, a certain quantity of futures in the underlying asset is accumulated at a certain strike, where both the quantity accumulated and at which strike depends on the market conditions on that fixing date. That is, it is the market conditions on that date which determine which of the predefined conditions included in the instrument will be activated and used to set the volume and strike for that date.

What are the predefined conditions?

You can optionally include up to 3 conditions, which are currently always based on the defined underlying contract. The available conditions are as follows:

The resultant portfolio of accumulated futures (with their relevant strikes) is then settled at maturity. It is of course important to note that at maturity the investor is obligated to buy all the accumulated futures (and the issuer to sell them).

The payout at maturity is calculated as follows:

Sum of volume * (asset price on expiry date - accumulated strike)

Where:

Sum of volume is the total volume accumulated on all the fixing dates together. On each fixing date the volume is set using the condition that is met on that date.

Accumulated strike is the weighted average price that is calculated as follows:

Total price on each fixing / the total volume on all fixings

Where the total price on each fixing is calculated as follows:

Number of futures accumulated on that date * set price for the matched condition

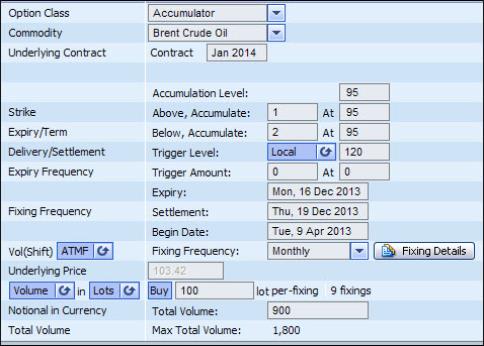

For example, you enter into an accumulator as seen in See "An Example of an Accumulator " with monthly fixings.

Figure 1: An Example of an Accumulator

In this example, if on any fixing date:

The spot is above the accumulation level (95) and below the knock out trigger (120), the buyer accumulates 100 futures (1 x 100) at a strike price of 95.

If the spot is below the accumulation level (95), the buyer accumulates 200 futures (2 x 100) at the strike price of 95.

The spot is above the trigger of 120, nothing is accumulated on that fixing date, i.e., that fixing is in effect “knocked out”.

Why enter into an Accumulator?

As a buyer, you may enter into an accumulator if you want to accumulate a position in a particular asset over a predefined period.

As such, you would enter into an accumulator rather than a different instrument if:

You have a very specific view of the price movement. That is, you think that the asset will trade between a certain price range (i.e., between the accumulation level and the trigger level) within the instrument's accumulation period, while the issuer speculates that the asset will fall below the accumulation level.

It is clear in the example in See "An Example of an Accumulator " above that you would enter into this accumulator if you think that the market will stay in a defined range (in the example, between 95 and 120) but you only have a slightly bullish view, i.e., that the rate will only slightly improve in your favour.

You want to fix a uniform strike (i.e., the price set in the relevant condition) for each fixing date over the instrument's lifetime. This is unlike a strip of forward contracts where each forward contract has a different strike price.

You want to base all fixings on the same futures contract.

You are looking to achieve a better rate on each fixing date than the prevailing forward rate in the market at the time of trading. You can achieve a better rate:

Because you are taking a risk on the final volume that will be accumulated. As such you are renumerated in the form of a discounted price compared with the forward price on the trade date.

This risk comes from the inclusion of 2 of the predefined conditions (and of course depends on how they are defined)-the Below condition and the trigger level.

Because you are taking a risk by inserting the local or global triggers, which can be set as knock out triggers.

Because you have defined that a higher volume of futures should be accumulated in the case of an out-of-the-money structure (if the Below condition is activated on the fixing date) than for an in the money structure (if the Above condition is activated on the fixing date).

As seen in See "An Example of an Accumulator " the risks are that:

If the price goes below the accumulation level (95) then you will have to buy a greater volume at an expensive price, i.e., (2 x 100) at 95, i.e., you may need to buy too much at an unfavorable price.

If the price goes up sharply (above 120) you will be unhedged on this date (for a local trigger) as no futures will be accumulated. If it was a global trigger, you will be unhedged on all future fixings as the instrument will in effect be knocked out.

However, the benefit is that if the future stays within the range of 95 and 120 you will buy at discount.

Defining an Accumulator in SDX Commodities & Energy

This instrument is supported in the pricer in the Portfolio page for all assets with the exception of OTC precious metals.

In the system, to define an accumulator (acc) the following parameters must be set:

Underlying contract

This is used as the underlying for the accumulation level and all defined conditions. It is also used to set the default expiry date of the instrument.

Accumulation level

This is the price that is then used on each fixing date to determine if either the Above condition or the Below condition is met.

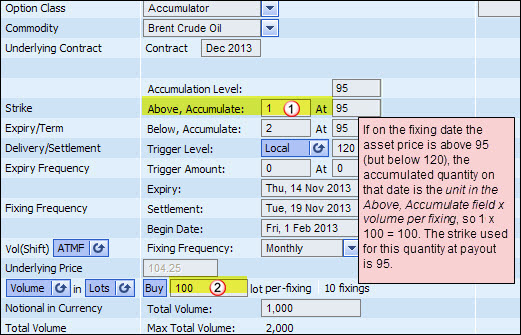

This condition defines the quantity of futures that will be accumulated (and the strike that will be used on the expiry date to calculate the payout for this accumulated quantity) if the underlying is above the accumulation level on the fixing date.

The quantity is calculated by multiplying the Above, Accumulate unit (as defined at 1 in See "An Example of an Accumulator Above Condition ") by the defined volume per fixing (as seen at 2 in See "An Example of an Accumulator Above Condition ").

| Figure 2: | An Example of an Accumulator Above Condition |

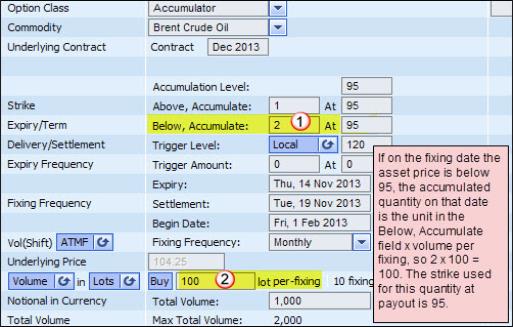

This condition defines the quantity of futures that will be accumulated (and the strike that will be used on the expiry date to calculate the payout for this accumulated quantity) if the underlying price is below the accumulation level on the fixing date.

The quantity is calculated by multiplying the Below, Accumulate unit (as defined at 1 in See "An Example of an Accumulator Below Condition ") by the defined volume per fixing (as seen at 2 in See "An Example of an Accumulator Below Condition ").

| Figure 3: | An Example of an Accumulator Below Condition |

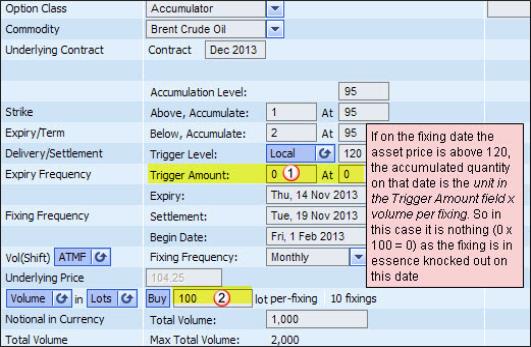

This condition defines the quantity of futures that will be accumulated (and the strike that will be used on the expiry date to calculate the payout for this accumulated quantity) if the underlying price is above the trigger level on the fixing date.

The quantity is calculated by multiplying the Trigger Amount unit (as defined at 1 in See "An Example of an Accumulator Trigger ") by the defined volume per fixing (as seen at 2 in See "An Example of an Accumulator Trigger ").

| Figure 4: | An Example of an Accumulator Trigger |

There are two types of triggers that can be used in the accumulator as follows:

Local trigger

The local trigger sets the underlying price that must be reached before this trigger condition is activated for this fixing date.

It can only be activated on a fixing date. Accordingly, if on a fixing date the underlying's price is above the defined trigger, the trigger condition for that particular fixing date is activated.

If required, you can set it as a knock out trigger.

Global trigger

The global trigger (which like the local trigger can also only be hit on one of the fixing dates) sets the price the underlying must reach before this trigger condition is activated. That is, if on one of the fixing dates the price is above the defined trigger, this condition is applied to this fixing date and all the remaining fixing dates.

If required, you can set it as a knock out trigger.

Regardless of which type of trigger is selected:

For an accumulator, the trigger level must be set above the accumulation level.

If the trigger condition is met on a fixing date, then the Above condition is no longer enabled for this fixing date.

The trigger can be used as a knock out trigger. To do this, you would set the number of units to be accumulated in the instance that the trigger condition is met to 0.

If it is a local trigger and the knock out is triggered on a fixing date, then nothing is accumulated for that fixing date only. However, if it is a global trigger and the knock out is touched on a fixing date, then its condition is automatically used on all the remaining fixing dates-the instrument is in effect then automatically knocked out, although of course any futures already accumulated before the knock out event will still be settled at maturity.

Begin date

You must define the start of the accumulation period.

By default this is set to the trade date. You can then edit it.

Expiry

You must define the end of the accumulation period.

By default the expiry of the instrument is set to the same expiry as that of a vanilla option based on the same underlying contract. You can then edit it.

Settlement

This is the date on which the payout is settled.

By default the instrument's settlement date is set to 3 business days after the expiry date. You can then edit it.

Fixing Frequency

You must define the fixing date frequency for the underlying sub-structures. This information, together with the data in the Begin Date and Expiry fields, is used to define the fixing date of each underlying structure (and therefore also its fixing date).

Volume per Fixing

The value defined here is used together with the unit set in the condition (Above, Below or Trigger) that is triggered on each fixing date. By multiplying them, you get the actual volume accumulated on that fixing date.

So for example if the Volume per Fixing is set to 50 and the condition triggered on a fixing date say you should accumulate 4 units, you will accumulate 200.

Buy <> Sell button

You can buy or sell the obligation to buy the accumulated futures.

Total Volume

This is the total amount of futures that you want to buy. It is calculated using the Above condition as follows:

Above Accumulate amount * volume per fixing * no. of fixings

Max Total Volume

This is the maximum amount of futures that you may have to buy, taking into account the three conditions (if they are defined).

This is calculated as follows:

max(Above Accumulate amount, Below Accumulate amount, Trigger Amount) * volume per fixing * no. of fixings