A TARN is a target redemption note.

It is important to understand that a TARN is not in itself an independent product, but rather it exists as an additional feature to an existing product. That existing product is actually a strip of structures, which generate both positive payouts and negative payouts (if there is more than one leg in each structure). The add-on part is that there is always a target redemption condition (or cap) added to the payout of the underlying structures. For a description of the structures currently available in SDX Commodities & Energy, see below.

The fixing dates of the TARN are the expiry dates of the underlying structures. If on any fixing date before the product's end expiry date the target redemption condition imposed on the positive payout is reached, the entire product is redeemed. That is, the rest of the product (including all legs of all remaining structures) ceases to exist. However, any positive payout (profits) or negative payout (losses) accumulated before the knock out event still need to be received/paid.

Currently in SDX Commodities & Energy only one type of target redemption condition can be placed on the payout, and that is the Accumulative payout cap.

With an accumulative payout cap, the sum of all payouts (also called the positive accumulated intrinsic value) that the buyer of the TARN can receive over the life of the contract is limited to a predefined limit (called the redemption target or maximum target). Once the limit has been reached, the contract ends.

In SDX Commodities & Energy, in the Target Redemption field you specify the redemption target after which the TARN terminates.

By default, the accumulative payout cap is applied to the sum of all positive payouts (also called the positive accumulated intrinsic value) received. That is, for the purposes of calculating whether the cap has been reached, only the positive payouts are taken into account; any payouts that have to be made were disregarded. In this type of instrument, the positive accumulated intrinsic value is not reduced by any losses suffered. So in a 2-leg structure, a loss incurred on any fixing date from the leg you sold is not set off against any positive accumulated intrinsic value. Or in other words, the positive accumulated intrinsic value is not lowered to take account of any losses incurred. This means that the buyer can reach the redemption target and see the contract end prematurely, but still have made a net loss over the life of the contract.

In a TARN, the actual payments calculated on each fixing date can be exchanged either after the expiry of each structure, or just once, after the last expiry date. Currently in SDX Commodities & Energy the payments can only be exchanged after the expiry of each structure.

When you enter into a TARN with an accumulative payout cap, you must also define how to treat the last payment if on a fixing date the target redemption is hit. You can choose any of the following definitions:

An exact TARN.

With an exact TARN if on a fixing date the target redemption is hit, then the payout is adjusted so as not to exceed the redemption target (and it becomes the last payment).

So on each fixing date, if using the predefined strike would result in the positive payout exceeding the target redemption, the system recalculates the notional that must be used. This is in order to ensure that the positive payout will equal and not exceed the redemption target. In such a situation, this last payment is known as a partial settlement.

A non-exact TARN.

With a non-exact TARN on a fixing date, even if using the predefined strike would result in the positive payout exceeding the target redemption, that predefined strike will nevertheless be used. Accordingly, with a non-exact TARN the sum of all positive payouts received by the owner of the TARN can exceed the redemption target.

Of course, if the target redemption is exceeded by a payment, that payment becomes the last payment and the entire instrument is terminated.

That the last payment is not to be made.

That is, if on a fixing date the target redemption is hit, then that payment is not made.

In SDX Commodities & Energy you define how to treat the last payment using the Last Payment radio buttons.

Select:

Capped by Redemption to specify an exact TARN.

Paid in Full to specify a non-exact TARN.

Nothing to indicate that the last payment should not be made.

Which underlying structures does SDX Commodities & Energy currently support?

Currently in SDX Commodities & Energy, the structures to which you can add-on a TARN are all based on Asian options although the actual number of underlying legs differs from structure to structure.

The supported structures are as follows:

A target redemption forward (TARF) has two underlying Asian options (each of which is referred to as a leg), one of which you buy and one of which you sell.

It is typically set up as a zero cost structure that enables the holder of the structure (the customer) to buy/sell a specified amount of a commodity, at a specified rate (that is typically better than the current market rate), on a set expiry schedule until the cap is triggered.

The customer effectively either buys a call and sells a put or sells a call and buys a put, where the strike (and expiry date) of each leg is always the same. This creates a synthetic forward, as the two simultaneous trades lock in the forward rate (or strike) that the counterparties will trade at in the future (on the expiry date) as one leg of the strategy will definitely be exercised.

In SDX Commodities & Energy, the notionals for a target redemption forward are automatically set to give you a participating forward. That is, where the notional of the leg you are selling is greater than the notional of the leg you are buying. You can of course manually override this default, but the participating forward aspect of the structure will give you leverage.

In See "Example of a Target Redemption Forward ", if on the structure's expiry date the average fixing rate calculated (i.e., the average of all the underlyings measured on each of the structure's defined fixing dates) is:

Higher than the forward rate specified in the contract in the Strike fields (i.e., 60), the customer buys a specified amount of the commodity as defined in the Volume1 field (i.e., 5,000) at that forward rate.

In addition, the positive accumulated intrinsic value is increased by an amount calculated as follows:

[Average fixing rate - strike] x amount defined in the Volume1 field

Lower than the forward rate specified in the contract in the Strike fields (i.e., 60), the customer buys a specified amount of the commodity as defined in the Volume2 field (i.e., 10,000) at that forward rate. The customer therefore suffers a loss. However, this loss is not detracted from the positive accumulated intrinsic value.

Figure 1: Example of a Target Redemption Forward

Target redemption one leg

A target redemption one leg (TARN1) is effectively an Asian strip with a TARN condition added. There is always one leg in this structure, either an Asian call or put option. The maximum profit from the option buyer's point of view is capped by the target redemption amount.

Target redemption three legs

A target redemption three legs (TARN3) has three underlying Asian options (each of which is referred to as a leg), one of which you buy and two of which you sell or one of which you sell and two of which you buy.

It is typically set up as a zero cost structure that enables the holder of the structure (the customer) to buy/sell a specified amount of one commodity, at a specified rate (that is typically better than the current market rate), on a set expiry schedule until the cap is triggered.

It is similar to the target redemption forward with the addition of an extra leg. The additional leg, which is also an Asian option, can be either of the following:

Sold

This leg makes the forward structure cheaper, but also caps the scope of the hedge (limiting the upside profit) should the value of the underlying rise.

Bought

This leg makes the forward structure more expensive because it limits the downside risk.

Target redemption pivot

A target redemption pivot (TARP) differs from a regular target redemption in that for some of its legs it also specifies knock out conditions that relate to the underlying price on each structure's expiry date. These knock out conditions are in addition to the cap on the cumulative positive payout that is common to all TARNs.

It is a strip of structures in which each structure is comprised of four Asian options as follows:

Option 1 is a Sell Put with Strike 1 and Volume 2.

Option 2 is a Buy Call with Strike 1 and Volume 1. In addition it has a European knock out trigger which is triggered if the underlying is above the defined pivot amount.

|

|

When a knock out condition occurs, only this option is knocked out and only for the current expiry. |

Option 3 is a Buy Put with Strike 2 and Volume 1. In addition it has a European knock out trigger which is triggered if the underlying is below the defined pivot amount.

|

|

When a knock out condition occurs, only this option is knocked out and only for the current expiry. |

Option 4 is a Sell Call with Strike 2 and Volume 2.

Target redemption inverse pivot

A target redemption inverse pivot (TARIP) structure differs from a regular target redemption in that for some of its legs it also specifies knock out conditions that relate to the underlying price on each structure's expiry date. These knock out conditions are in addition to the cap on the cumulative positive payout that is common to all TARNs.

It is a strip of structures in which each structure is comprised of four Asian options as follows:

Option 1 is a Sell Put with Strike 1 and Volume 2.

Option 2 is a Buy Put with Strike 2 and Volume 1. In addition it has a European knock out trigger which is triggered if the underlying is outside the range defined by the Strike 1 and Pivot values.

|

|

When a knock out condition occurs, only this option is knocked out and only for the current expiry. |

Option 3 is a Buy Call at Strike1, Volume1. In addition it has a European knock out trigger which is triggered if the underlying is outside the range defined by the Pivot and Strike 2 values.

|

|

When a knock out condition occurs, only this option is knocked out and only for the current expiry. |

Option 4 is a Sell Call with Strike 2 and Volume 2.

Why are TARNs used?

Broadly speaking, a TARN reduces the cost of a structure as the buyer's earning potential is limited. The primary advantage of a TARN is that it can be built as a zero-cost structure (if there are two legs) and offers a better-than-market rate. In such cases, TARNS are used to:

Express a view on the movement of a market rate, at lower cost than a vanilla.

Hedge a position at a rate significantly more favorable than the prevailing market rate (forward rate), typically when the corporation did not manage to meet its budget rate.

Protect a cash flow by setting the payment dates and amounts as required.

TARNs in which the customer buys and sells commodities (obviously only in a 2-leg structure) offer better-than-market rates for two reasons:

Profits are limited, losses are unlimited.

The cumulative positive payouts the customer can receive is limited, while the losses that can be suffered are unlimited. Thus a more preferable rate can be obtained at a given cost than could be obtained if the upside potential was not limited.

Leveraging uses different notionals for the leg you are buying and the leg you are selling. By setting the notional for the sold leg higher than for the bought leg, the potential for losses is increased relative to the potential for profits, and thus a more preferable rate can be obtained at a given cost than could be obtained if the notionals were equal for both legs.

For example, consider a TARN contract in which the customer sells a particular commodity for another at regular intervals, hoping to receive a higher than market value for the commodity being sold.

Typically (but not necessarily), the amount of commodity that must be sold when the market rate is higher than the strike (and the customer is thus suffering a loss) is larger than the amount of commodity that must be sold when the market rate is lower than the strike (and the customer is thus profiting). This leverage lowers the cost associated with higher strike rates.

|

|

This is only true for structures that contain more than one leg, something that is not yet supported in SDX Commodities & Energy. |

What do you need to take into account before entering into a TARN?

As a result of the cap:

Whereas there is a limit to the cumulative positive payout that you can earn, the total amount that you can lose over the life of the contract on the leg you sell (if each structure has two legs) is unlimited.

Moreover, if you enter into a TARN with an accumulative payout cap which is only applied to the positive payouts, the positive accumulated intrinsic value is not reduced by any losses suffered. That is, if there are 2 legs in each structure, a loss incurred on any fixing date from the leg you sold is not set off against any positive accumulated intrinsic value. Or in other words, the positive accumulated intrinsic value is not lowered to take account of any losses incurred. This means that the buyer can reach the redemption target and see the contract end prematurely, but still have made a net loss over the life of the contract.

If a customer enters into a TARN for hedging purposes, once the redemption target has been met, the TARN terminates and the buyer loses the hedge. If the customer earns high profits early on in the contract, the redemption target will be met quickly and the contract will terminate long before the scheduled expiry, leaving the customer unhedged.

In addition, if it is a 2-leg structure, the TARN is also made more risky by the fact that the underlying structure is often created as a participating forward, i.e., the notional of the leg you sell is greater than the leg you buy, in order to give leverage. Although leverage lowers the cost of the structure and can give a better market rate, as a result, the amount of commodity that will need to be sold if the market rate is higher than the strike (and you are thus suffering a loss) is larger than the amount of commodity that can be sold if the market rate is lower than the strike (and you are profiting).

Pricing TARNs in SDX Commodities & Energy

When pricing a TARN in the system note the following:

A TARN can only be priced in the Single Option page.

Once you have defined the instrument in the pricing page, using the Expiry Dates & Rates window (accessed by clicking the Expiry Dates & Rates button), for each underlying structure you can see the expiry date, settlement date, begin date, end date, strike, volume and underlying swap, as well as edit its settlement date, strike and/or volume.

You can define the direction of the underlying legs of the existing product, as well as that of the actual target redemption instrument itself. By default the direction of the target redemption instrument is set to Buy, but you can choose to set it to Sell instead. You do this using the Buy <> Sell button next to the Volume fields.

|

|

Setting the direction of the overall instrument to Sell is not the same as simply flipping the Buy/Sell direction of the underlying legs. |

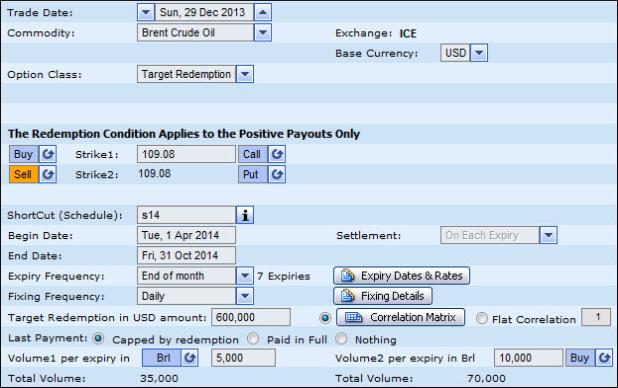

To price a TARN in SDX Commodities & Energy

| 1. | From the Option Class dropdown list, from the Target Redemption list select the structure to which you want to add a TARN. |

| 2. | Specify the trade date. |

| 3. | Specify the commodity. |

| 4. | Specify each of the fields listed below. |

The strike.

The duration. This automatically sets the begin date and end dates.

The expiry frequency.

The fixing frequency.

The volume(s) per expiry. This automatically sets the notional amounts in the base currency.

The trigger condition(s) where relevant.

|

|

The strike and volume can then be specified per payment period in the Expiry Dates & Rates window, accessed by clicking the Expiry Dates & Rates button |

| 5. | In the Target Redemption field, specify the target amount in the base currency. |

| 6. | Choose a correlation method. |

For a description of the two available methods see the online help.

| 7. | Choose a last payment method. |

| 8. | Click Calculate. The results are displayed. |