The value of any given trade depends, among other elements, on whether you choose to apply the cash collateralization method or, alternatively, to not collateralize the trade at all. This is because the collateralization method necessarily affects both the curve from which the discount factors1 are taken as well as the projected rates (which are also known as implied rates).

If you:

Choose to not collateralize the trade, by default SD uses the pure LIBOR curve (from the trade currency's default yield curve2 or from any of the other LIBOR indexes available for that currency) for both discounting and to calculate the implied rates.

Choose to use the cash collateralization method, this means you will discount your cash flows using the OIS curve and project cash flows using co-bootstrapped LIBOR-OIS curves, and not using pure LIBOR discounting or pure LIBOR projections.

In addition, if you choose to apply this method for any given instrument, it is important to note that there is also another issue to take into account—that you may be pricing this trade in a currency that is different from the collateral account currency, for example, you may be pricing a EUR swap when your collateral account currency is managed in USD, or you may be pricing an instrument on BRR (a currency for which there is no OIS curve) with a collateral account currency set to EUR.

If this is the case, the pricing will also need to take into account the fact that the collateral is earning interest based on a different overnight rate from that of the trade currency or that the trade currency does not have an overnight rate. In order to do this, the system prices the instrument taking into account all of the following elements—the OIS curve of the collateral account currency, the Libor curve for both the collateral account currency and the trade currency, and the cross currency basis spreads between those two currencies.

In addition to supporting the regular cash collateralization method (where you can optionally choose a collateral account currency that is different from the trade currency), there is also support for a variation of the cash collateralization method, known as CTD (cheapest-to-deliver) collateralization. This method lets you select a number of collateral account currencies for the given instrument.

Why would you want to choose multiple collateral account currencies? It has now become quite commonplace when defining a CSA3 (or credit support annex) to include a number of collateral account currencies. This is because entering into a multi-currency CSA allows the counterparty posting the collateral to choose (at regular intervals) the collateral account currency which will give the highest return on the posted collateral, i.e., the currency with the highest forward collateral rate.

How does CTD collateralization work in SD? To price this instrument, SD calculates the optimal discounting curve based on the defined currencies.

To do this, it uses the current market data in order to calculate which of the defined multiple currencies will be the best (i.e., the cheapest) collateral account currency for each 3 month period over the life of the instrument. In each period the cheapest currency is the one with the highest interest rates, which will result in a lower discount factor. It then uses this information to build the discounting curve, taking the “best” currency for each 3m period.

|

|

If you choose either cash collateralization method for an instrument:

|

In recent times it has become more commonplace to use the cash collateralization method in the pricing and revaluation of IR deals. This is because in present market conditions, a large number of trades are now subject to regular collateral calls4, daily in most cases; and for any trade that is 100% cash collateralized with daily collateral calls, you will necessarily use the cash collateralization method. This is because the balances which are built up as a result of these collateral calls are saved in a collateral account and subsequently earn interest—not using the LIBOR rate, but at the relevant overnight rate, e.g., the Fed Funds rate, the EONIA rate, etc., which themselves form the basis of the relevant currency’s OIS curve.

In SDX Interest Rates, by default for each instrument (with the exception of the OIS swap5) the system does not use collateralization, and it uses the trade currency’s pure LIBOR curve (from the relevant default yield curve) for discounting and to calculate the implied rates—so, for example, for USD it uses the 3m yield curve, for EUR it uses the 6m yield curve, etc.

However, depending on both the selected currency and the selected instrument, a user can change this setting, to use any of the other LIBOR indexes available for the trade currency (instead of using its default yield curve) or to use the cash collateralization method (either the regular cash collateralization method or the variation known as CTD collateralization6).

For more information on defining which method is used, see Controlling Which Collateralization Method Is Used.

In addition, if you choose to not collateralize the trade, then you can also instruct SD to use the co-bootstrapped LIBOR-OIS curves instead of the pure LIBOR curve. This setting, unlike the collateralization method itself (which is set per currency in the Customize window or per instrument in the pricing page), is controlled globally per user. For more information see Controlling the Setting for the Non-collateralization Method.

Controlling Which Collateralization Method Is Used

For each currency there are two ways to control which collateralization method is used, if at all, and therefore which curves the system uses to take the discount factors and to calculate the implied rates.

|

|

|

The two ways are as follows:

Setting the default collateralization method per currency.

By default, for each currency the system does not use Collateralization, and therefore takes the discount factors and calculates the implied rates using the currency’s relevant default yield curve. However, you can then control the default collateralization method used per currency, and save this setting permanently in the system into either your MyProfile profile or a group profile.

You do this in the Customization window | Default Settings | Currency tab using the Collateralization radio buttons.

Once you have set the default collateralization method for a currency, if you have selected either the cash collateralization in trade currency method or to not use collateralization at all, then you can then apply this setting to all other currencies7. You do this by clicking the Apply to all Currencies button. If you use this functionality, it is important to note that:

The system will then apply this setting to all currencies. However, note that to save this setting permanently in the system for all currencies you must save the profile.

If you have chosen the cash collateralization in trade currency method, it is only applied to currencies with an OIS curve.

If you have chosen the currency's default yield curve, for each currency the system will use that currency's own default yield curve. So for USD this will be the 3M LIBOR, for DKK the 6M CIBOR, etc.

It is important to note that regardless of whichever default setting you choose for a currency, you can subsequently always manually override this default setting in the pricing page itself using each instrument’s Collateralization button.

|

|

The default method set here for each currency, using the Collateralization radio buttons, also determines the collateralization method used in your Excel spreadsheet—if you have inserted SD’s Excel add-in and are pricing supported instruments there. That is, when you price a supported instrument using the SD pricing model in an Excel spreadsheet, SD uses the default collateralization method set for its currency using the Collateralization radio buttons. For more information on working with the Excel add-in see Adding SD Functionality into Excel. |

Manually in the pricing page.

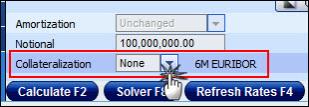

In the pricing page for each defined instrument, by default the system uses the selected currency’s default collateralization method as set in the system8. However, you can then manually edit the default collateralization method (and therefore the discounting curve) used for each instrument. You do this using the Collateralization dropdown list as seen in Figure 1.

| Figure 1: | Defining Which Collateralization Method Is Used to Price the Current Instrument |

You should be aware that:

Whether the Collateralization dropdown list is enabled at all and, if it is, which options are available in it, is dependent on both the selected instrument and currency. For example, the collateralization feature is currently not supported for the following instruments—structured swaps, CMS instruments, FX-linked instruments, and any instrument which contains more than one currency, e.g., UDI swap or the cross currency swap. In addition, even for a supported instrument you will not see the CTD option if there is no OIS curve available for the defined currency, e.g., EUL or BHD.

When you save a deal or portfolio, the collateralization method as set in the pricing page is also saved together with it. Accordingly, when you next open it, it opens by default with the collateralization method it was saved with9. Of course, you can then manually edit the collateralization method if relevant.

If you send the deal to another user using the Send button, the collateralization method as set in the pricing page is sent together with the deal. So when the user opens the deal the system will use the collateralization method selected by you.

If you are pricing a EUR, GBP or JPY swaption, the collateralization setting also controls which volatility surface the system will use. For more information, see Toggling Between the Volatility Surface for Collateralized and Non-Collateralized Swaptions.

In the Portfolio page you can choose which method of collateralization to use per instrument. This gives you great flexibility when defining your portfolio. For example, if the portfolio contains some instruments that support OIS discounting, e.g., a vanilla swap, and some that do not support it, e.g., a callable swap, you can apply OIS discounting to the relevant instruments.

So what can you set in the pricing page?

In the pricing page you can tell SD:

To not apply cash collateralization and to instead use LIBOR discounting from the currency’s default yield curve.

To do this, from the Collateralization dropdown list you select None. Alternatively, from this dropdown list you can instead select Custom and then select the currency’s default yield curve.

To not apply cash collateralization method and to instead use LIBOR discounting from one of the trade currency’s non-default yield curves.

To do this, from the Collateralization dropdown list you select Custom and then select the relevant non-default yield curve for the trade currency.

To use the regular cash collateralization method.

If the collateral account currency is the same as the trade currency, you can do this in one of two ways as follows—you can simply select Cash from the Collateralization dropdown list (by default SD sets the collateral account currency to the trade currency) or you can select Custom from the Collateralization dropdown list and then select OIS10, whereby SD automatically assumes that the collateralization account currency is the same as the trade currency.

If the collateral account currency is not the same as the trade currency (or if the trade currency does not have an OIS curve), you must first select Cash and then, using the dropdown list as seen at 1 in Figure 2, you must define the collateral account currency.

| Figure 2: | Tell SD if the Collateral Account Currency Is Different from the Trade Currency |

To use the CTD collateralization method11.

This method lets you select a number of collateral account currencies for the given instrument.

You apply this method by first choosing the CTD collateralization method from the Collateralization dropdown list (as seen at 1 in Figure 3). Once you have done this, a dropdown list then appears (as seen at 2 in Figure 3) where you can select the multiple collateral account currencies for this instrument.

| Figure 3: | Defining a Number of Collateral Account Currencies |

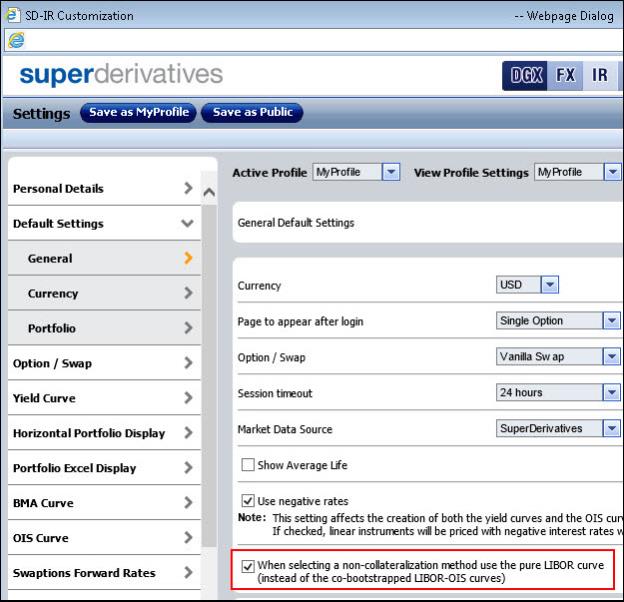

Controlling the Setting for the Non-collateralization Method

The value of any given trade depends, among other elements, on whether you choose to apply the cash collateralization method or, alternatively, to not collateralize the trade at all. This is because the collateralization method necessarily affects both the curve from which the discount factors are taken as well as the projected rates (which are also known as implied rates).

If you choose to not use collateralization, SD automatically uses the pure LIBOR curve (from the trade currency's default yield curve or from any of the other LIBOR indexes available for that currency) for discounting and to calculate the implied rates.

However, you can instruct SD to use the co-bootstrapped LIBOR-OIS curves instead. If you do this, SD will then use the co-bootstrapped LIBOR-OIS curves for discounting and to calculate the implied rates.

If you do change this setting, it will necessarily affect the pricing of the trades. In addition, it will also affect the calculations in the system involving forward rates and/or discounting as follows:

The forward rates displayed in the Swaption Forward Rates page and the Cap Term Structure page.

The strikes displayed in both the Volatility Surface pages.

You control this setting using the checkbox in the Customize window > Default Settings tab > General tab as seen in Figure 4.

If you uncheck the checkbox, SD will use the co-bootstrapped LIBOR-OIS curves instead of the pure LIBOR curve.

Figure 4: Setting the Method for the Non-collateralization Method