In the pricing page, you specify the notional on which interest payments are to be paid in the Notional field. By default this sets the same notional for each underlying coupon in the structure.

Subsequently, if relevant, in the instrument’s Cash Flow Dates page (Working With the Cash Flow Dates Window) you can then adjust the notional on which interest payments are to be calculated for each individual coupon.

In the Cash Flow Date page you can manually adjust the notional for each payment by simply editing the relevant amount in each row. For more information on how to do this see Manually Adjusting Values for Individual Coupons.

However, you can also instruct the system to adjust the notionals for you using a number of different methods accessed via the Notional Per Fixing dropdown list.

|

|

This dropdown list is only displayed if the calculation of the current instrument supports changing the notional per coupon. |

Why is this useful? Being able to automatically amortize (decrease) or accrete (increase) the notional for individual coupons/caplets/floorlets lets you use these options to effectively hedge a swap, option or a position which is itself amortizing or accreting. For example, a customer has a floating rate loan such as a mortgage. Because the notional on which the customer is paying the floating interest rate decreases by a certain amount each month, the customer also wants to ensure that the notional of the hedge will amortize as well (this will reduce the notional of the hedge).

Similarly, you may want to adjust the notional using an algorithm. Consider a borrower who borrows an amount from a bank and is required to repay that amount in a certain number of installments, together with regular interest rate payments on the outstanding amount. The loan defines a fixed interest rate. The borrower would like instead to switch to a floating rate, and thus wants to enter into a fixed-floating interest rate swap.

To price such a swap, you have to take into the account the fact that the notional on which the borrower pays interest reduces each expiry because of the installments that are repaid. Although you could adjust the notional values for all expiries manually in the Cash Flow and Dates window, you can instead tell the system to automatically calculate the notionals using the same algorithms as commonly used by lending banks, i.e., a serial loan or an annuity loan.

From the Notional per Fixing dropdown list you can choose any of a number of methods.

|

|

In the Portfolio page, if you have chosen to view the page in the horizontal format in order to change the amortization type for a vanilla swap, general swap, cap/floor and general cap/floor see Setting an Amortization Type in the Horizontal View of the Portfolio Page. |

The available methods are as follows:

Unchanged

This sets all the notionals to the amount in the first notional field. This is the default setting.

Decrease

This automatically decreases (amortizes) the notional of each coupon by a fixed amount or percentage.

When you choose this method and you want to define the shift between coupons as a percentage, you can define the percentage with up to 2 decimal points.

|

|

For a swap, if you change the notionals of one of the leg's coupons using the Decrease option, when you then click the Accept button or the Calculate button, the system asks if you want to automatically apply those changes to the other leg as well. This functionality is available as long as either of the following circumstances are true:

|

Increase

This automatically increases (accretes) the notional of each coupon by a fixed amount or percentage.

When you choose this method and you want to define the shift between coupons as a percentage, you can define the percentage with up to 2 decimal points.

|

|

For a swap, if you change the notionals of one of the leg's coupons using the Increase option, when you then click the Accept button or the Calculate button, the system asks if you want to automatically apply those changes to the other leg as well. This functionality is available as long as either of the following circumstances are true:

|

Annuity Loan

For a vanilla swap, general swap, cross currency swap, swaption, cap/floor, general cap/floor and loan instruments you can choose an annuity loan method of determining the notional of each coupon.

|

|

|

This method uses an amortization algorithm usually associated with mortgage payments. In this type of amortization, the borrower pays the lender a fixed amount (the loan repayment) in each period (i.e., on the loan repayment dates). While the actual loan repayment—which consists of an interest payment and a principal repayment—paid at the end of each period remains fixed1, i.e., it is a constant annuity, the allocation of that amount to principal payments and interest payments differs for each period—as time progresses the interest payment component reduces and the principal repayment component increases. The notional at the first expiry represents the total amount borrowed.

This type of amortization is usually used to hedge an annuity amortized loan.

With this method you define either an interest rate or amount which is used to determine the loan repayments on the given loan repayment dates, which in turn determine the notional per coupon. Alternatively, you can use a loan repayment schedule (for determining the notional of each of the coupons) based on zero cost annuity.

That is, you can specify how to determine the loan repayments in any of the following three ways. You can:

Instruct SDX Interest Rates to calculate the fixed rate/payment that will ensure that the notionals will be based on zero cost annuity (while at the same time ensuring that the borrower pays fixed payments for all expiries).

|

|

This method is only available for a vanilla swap, a general swap, a cross currency swap and a swaption’s underlying swap. |

To do this, type Zero Cost in the Of field as seen in Figure 1.

| Figure 1: | Use “Zero Cost” to Ensure that the Swap Will Be Zero Cost |

It does not matter if the toggle button is set to Percent or Amount—the amortization is performed the same regardless. You must then click the Calculate button to calculate notional values for all expiries.

Specify the fixed interest rate/annuity rate to be paid.

SDX Interest Rates will then amortize the notionals in such a way as to ensure that the borrower pays a fixed payment each expiry, i.e., the principal payment amount + interest payment (which is the fixed rate you specified x the outstanding notional).

To do this, enter your required fixed rate in the Of field and set the toggle button to Percent. You must then click the button to calculate notional values for all expiries.

|

|

If you specify a fixed rate other than the rate SDX Interest Rates calculates as the zero cost rate, the swap will have a non-zero NPV. |

Specify the fixed payment/annuity amount to be paid.

SDX Interest Rates will then amortize the notionals in such a way as to ensure that the borrower pays the fixed amount you specify each expiry. SDX Interest Rates will then calculate the fixed interest rate to be paid on the outstanding notional.

To do this, enter your required fixed payment in the Of field and set the toggle button to Amount. You must then click the Calculate button to calculate the notional values for all expiries.

|

|

If the fixed rate is other than the rate SDX Interest Rates calculates as the zero cost rate, the swap will have a non-zero NPV. |

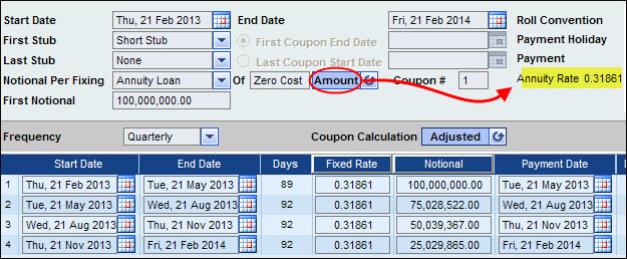

For example, the table below was created by setting the initial notional to 1m, and then selecting Annuity Loan from the Notional Per Fixing dropdown list and specifying the interest rate as the zero cost rate. The loan was specified to be repaid over one year in four installments. SDX Interest Rates calculated that the zero cost interest rate was 2.9521%.

| Figure 2: | Coupon Notionals Adjusted by the Annuity Loan Method |

At the:

First expiry, the notional is 1m. The interest paid is 2.9521% x 1m x 91/360 = 7,462, as shown in the Cash Flow column. The principal amount paid back is the change in notional between the first and second expiries, i.e., 1m - 752,781 = 247,219. The total that the borrower paid at the first expiry is thus 7,462 + 247,219 = 254,681.

Second expiry, the notional is 752,781. The interest paid is 2.9521% x 752,781 x 90/360 = 5,556, as shown in the Cash Flow column. The principal amount paid back is the change in notional between the second and third expiries, i.e., 752,781 - 503,656 = 249,125. The total that the borrower paid at the second expiry is thus 5,556 + 249,125 = 254,681, which is the exact same amount as paid at the first expiry.

Third and fourth expiries, the interest payment and principal repayments are calculated in the same way as described above. In both cases the rate of interest paid is 2.9521% and the total of the interest rate payments and principal repayments is the same, i.e., 254,681.

In addition, note that if you choose to determine the notional using the annuity loan method, as long as you choose to determine the notional for each successive period by an amount (rather than by a percentage), or if you choose to set the notional repayment schedule according to the zero cost annuity rate (whether in the percentage or amount mode as seen in Figure 3), then the system also shows the resultant annuity rate.

Figure 3: Annuity Rate Is Displayed If You Reduce the Notional by an Amount in the Annuity Loan Method

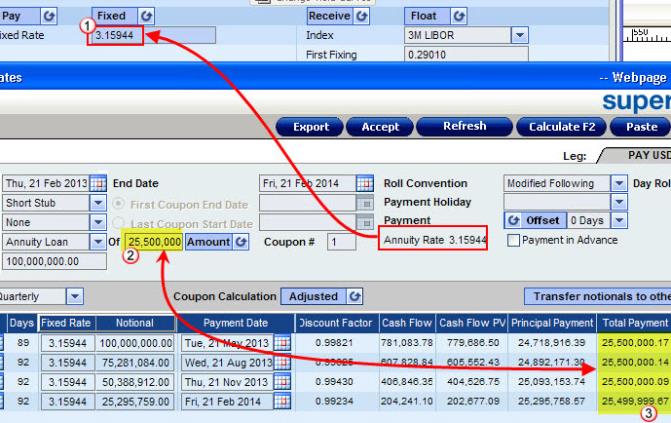

Why is being able to see the annuity rate useful? This functionality is useful as it lets you overwrite the fixed rate of the deal (as seen at 1 in Figure 4) with the calculated annuity rate. This is necessary if you want to achieve constant payments for each coupon which are also equal to the defined amount per coupon (as seen at 2 in Figure 4).

Note that the payments for each of the coupons are displayed in the Total Payment column, as seen at 3 in Figure 4, and that each of these payments consists of the interest and principal payment for that coupon.

Figure 4: You Can Overwrite the Deal’s Fixed Rate with the Calculated Annuity Rate

Serial Loan

For a vanilla swap, general swap, cross currency swap, swaption, cap/floor, general cap/floor, loan and double period loan instrument you can choose a serial loan method of changing the notionals.

|

|

|

This method uses an amortization algorithm that reduces the notional by the same fixed amount each expiry. The amount is calculated by the system to ensure that the notional is repaid by the end of the swap.

It is calculated as follows:

Notional / number of periods

SDX Interest Rates also calculates the fixed rate to be paid at each expiry that will ensure a zero NPV.

For example, the table below shows the notional as reduced using the serial loan option. The initial amount borrowed was 1m, and that amount is to be paid over one year in four payments.

| Figure 5: | Notionals Adjusted By the Serial Loan Method |

As can be seen, the notional is reduced each expiry by a fixed amount of 250,000. Note that the notional at the last expiry is 250,000—paying the fixed amount of 250,000 at this expiry repays the loan.

It is also important to note that if you choose the serial loan method of adjusting, the method will be applied to both of the swap’s legs. So for any supported swap or swaption, if there are a different number of coupons per swap leg and you choose the Serial Loan method of amortization, the system in effect amortizes the notional of the leg with fewer coupons and then simultaneously transfers these notionals to the leg with more coupons.

For example, you enter into a 1Y swap on 1 April 2010 with a semi-annual frequency on the left leg and a quarterly frequency on the right leg. Once you choose the Serial Loan method and apply it by clicking the Calculate button, the left leg, which has less coupons, will automatically have amortization applied to each coupon (i.e., every six months). So as seen in Figure 6, the notional of the first coupon will be 10,000 and of the second coupon will be 5,000. The amount for each coupon on the left leg is then automatically transferred to the relevant coupons on the right leg (i.e., the coupons that fall in the same period). So the amount of 10,000 is transferred to all the right leg coupons up to 5 October 2010; the amount of 5,000 is transferred to all the right leg coupons between 5 October 2010 and 5 April 2011.

| Figure 6: | How a Serial Loan Amortization Is Applied to a Swap with Uneven Legs |

Custom

If you manually adjust any of the coupons’ notionals, the system automatically sets the Notional Per Fixing dropdown list to Custom.

In addition you can defer the notional adjustment to a specific coupon. See Deferring Notional Adjustment to a Specific Coupon.

|

b |

|

To adjust the coupons’ notionals automatically:

| 1. | In the pricing page define the instrument including its notional. |

| 2. | Click the Cash Flow & Dates button. The Cash Flow and Dates window opens. |

| 3. | From the Notional per Fixing dropdown list select the required notional adjustment method. The coupon area at the bottom of the window is disabled, and in addition, depending on the method chosen extra fields are displayed. |

| 4. | Fill in the extra fields as necessary. |

| 5. | To display the new notionals and recalculate the coupons results accordingly, click the Calculate button. The notionals and cash flows are recalculated as required. |

| 6. | Click Accept. The changes are saved and the pricing page is updated. The Notional field no longer shows the notional value; instead it shows the Variable button, and the Current Notional field is added. |